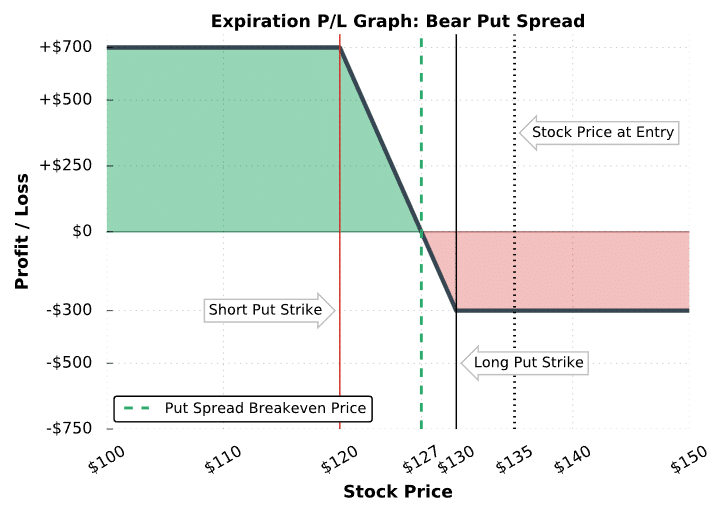

This particular put spread is out-of-the-money because the 130 and 120 puts are both out-of-the-money. As a result, the put spread has a probability of profit less than 50% because the stock price must fall below 130 for the position to have any value at expiration.

Additionally, the maximum profit potential is $700, and the maximum loss potential is $300, which also suggests a lower probability of profit because the reward is greater than the risk.

The following table describes various scenarios of this bear put spread position at expiration:

Stock Price At or Below the Short Put Strike Price (At or Below $120):

Both options of the put spread are fully in-the-money, and since the put strikes are $10 apart, the spread is worth its maximum value of $10 at expiration. With an initial purchase price of $3.00, the put spread buyer realizes the maximum profit potential of $700: ($10 spread price at expiration – $3 spread purchase price) x 100 = +$700.

Stock Price Between the Short Put Strike Price ($120) and the Breakeven Price ($127):

The long 130 put expires with more intrinsic value than the $3.00 purchase price of the spread. Because of this, the put spread buyer is profitable at expiration.

Stock Price At the Breakeven Price ($127):

The long 130 put is worth exactly $3.00 at expiration, and the 120 put expires worthless. As a result, the 130/120 put spread’s final value is $3.00. Since the spread was initially bought for $3.00, the trader realizes no profits or losses.

Stock Price Between the Breakeven Price ($127) and the Long Put Strike Price ($130):

The short 120 put expires worthless, and the long 130 put expires with less than $3.00 of intrinsic value. As a result, the 130/120 put spread’s final value is less than $3.00, which results in losses for the buyer of the put spread.

Stock Price At or Above the Long Put Strike Price ($130):

Both the 130 and 120 put expire worthless, resulting in a $200 profit on the short 120 put, and a $500 loss on the long 130 put. The net loss is $300, which is the maximum loss potential of a spread purchased for $3.00.

Nice job! You know the basics of the bear put spread strategy.

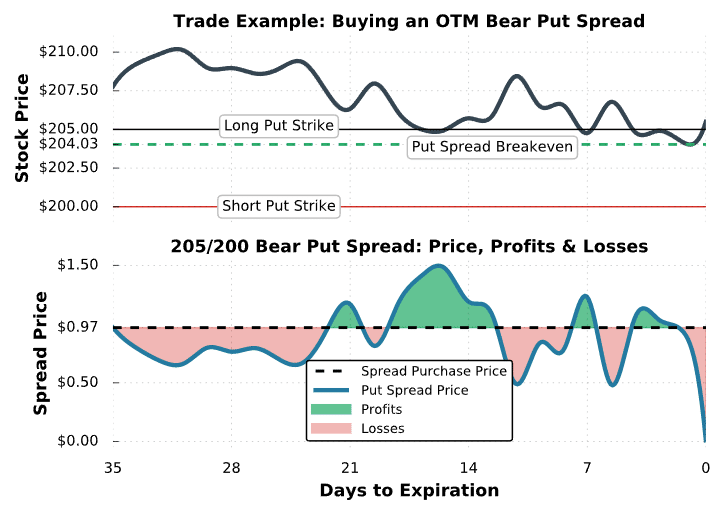

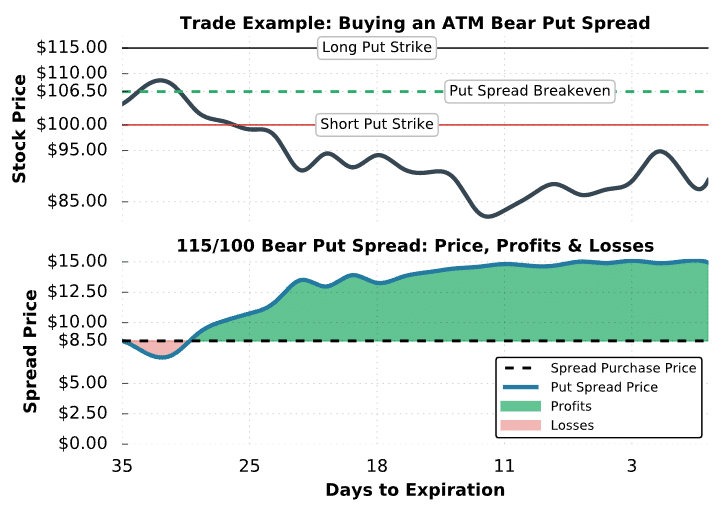

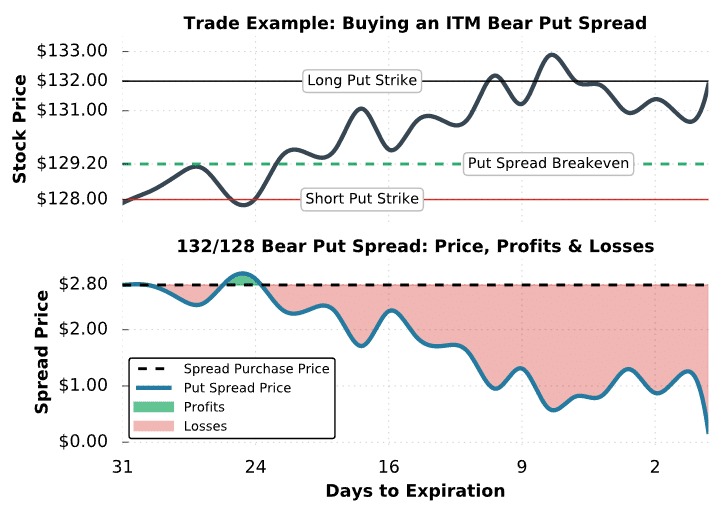

In the next section, we’ll look at real trade examples to show you how the strategy has performed over time in different scenarios.

(1)")