(1)")

Instead of just looking at the results of holding the short straddles to expiration, we’ll examine the usage of stop-losses as well to see if closing losing trades has improved the strategy’s performance over time.

NOTE: as opposed to a stop-loss order, a stop-limit orders guarantee a fill price.

Study Methodology

Product: S&P 500 ETF (SPY)

Expiration: Standard monthly cycle closest to 60 days to expiration (60 DTE).

Trade Setup: Sell the at-the-money call and put.

Management: None (hold to expiration), -50% loss, -100% loss, -150% loss.

Next Entry Date: First trading day after previous trades were closed.

Stop-Loss Example

To make sure you understand the stop-loss calculations, here are some examples:

Initial Straddle Sale Price: $10

-50% Loss: Straddle price increases by 50% to $15.

-100% Loss: Straddle price increases by 100% to $20.

-150% Loss: Straddle price increases by 150% to $25.

The stop-loss is just the percentage increase over the initial sale price that is used as a trigger to close the trade.

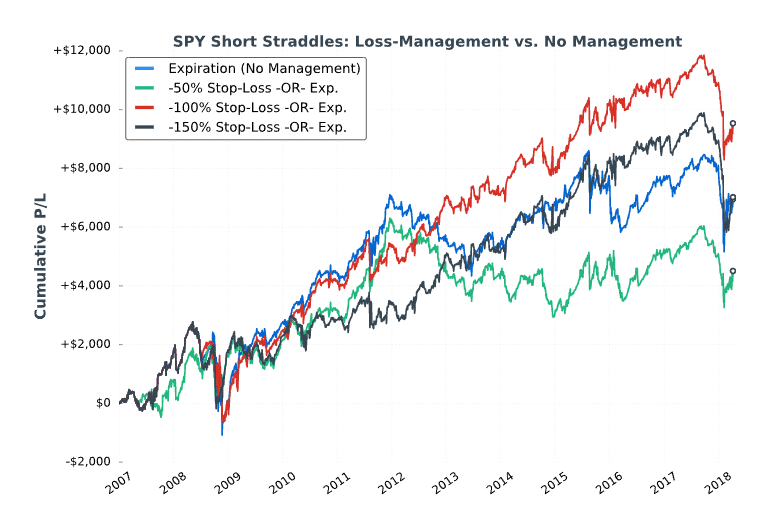

SPY Short Straddles: Taking Losses

Here are the results of the first study:

*Please Note: Hypothetical computer simulated performance results are believed to be accurately presented. However, they are not guaranteed as to the accuracy or completeness and are subject to change without any notice. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have been under or over compensated for the impact, if any, or certain market factors such as liquidity, slippage and commissions. Simulated trading programs, in general, are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any portfolio will, or is likely to achieve profits or losses similar to those shown. All investments and trades carry risk.

Compared to holding to expiration, implementing a stop-loss that was not too tight helped smooth out strategy returns. By using the smallest stop-loss and closing trades when the loss reached 50% of the premium received, the returns were choppy and inconsistent over the test period.

Visually, the best-performing approach was to use a -100% stop-loss, which means the short straddles were closed if the price doubled from the initial entry price.

With that said, all approaches suffered significant losses in February of 2018, which highlights the importance of keeping risk in mind before selling straddles.

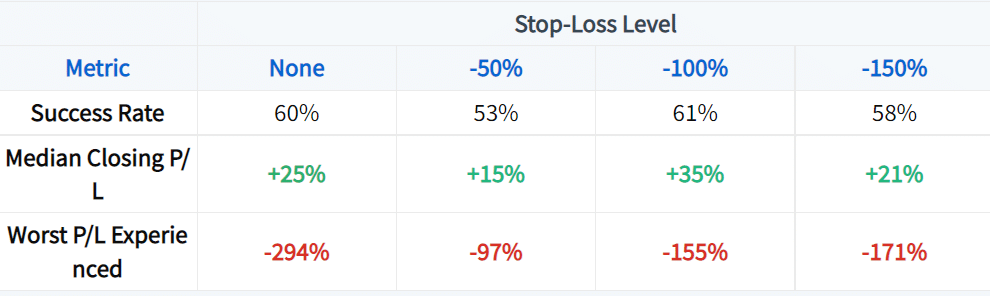

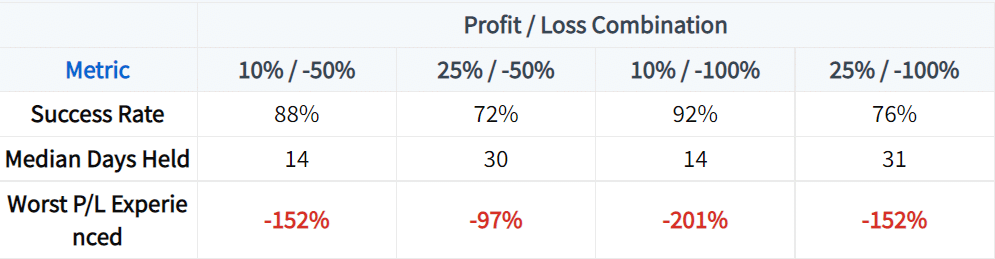

Here are some performance metrics related to each management approach:

Not many of the straddles reached the -100% P/L level, but the same percentage reached the -100% and -150% P/L levels. The data shows us that almost all of the straddles that reached the -100% loss level also reached the -150% loss level. The data suggests that using a stop-loss of -100% is strategically better than using a slightly wider stop-loss of -150%.

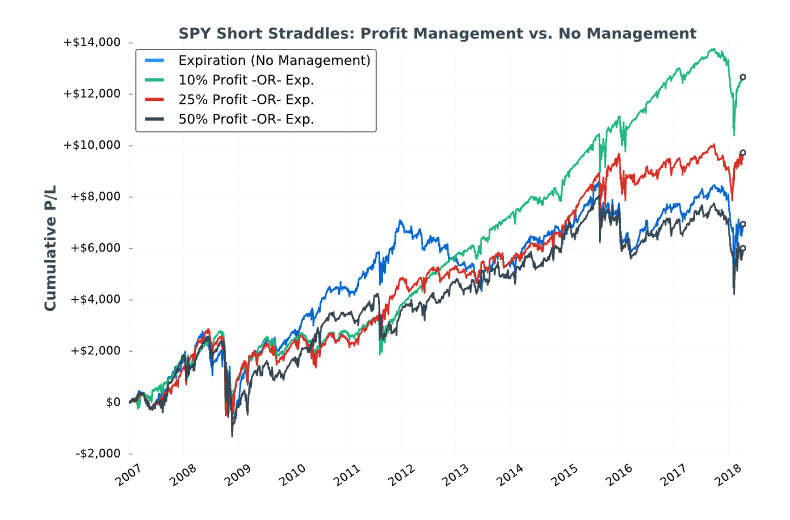

SPY Short Straddles: Taking Profits

Now that we’ve explored the usage of stop-losses when selling straddles, let’s look at the historical performance implications of closing profitable straddles early. The preferred order type to do this is the limit order.

We’ll use the same methodology as before:

Sell an at-the-money SPY straddle in the expiration closest to 60 days.

Management: None, 10% Profit Target, 25% Profit Target, 50% Profit Target.

Next Entry Date: First trading day after previous trades were closed.

For instance, if a straddle was sold for $10, a 10% profit would be reached when the straddle’s price decreased to $9 (a 10% decrease from the entry price). A 25% profit would be reached when the straddle’s price decreased to $7.50 (a 25% decrease from the entry price).

Here were the results:

*Please Note: Hypothetical computer simulated performance results are believed to be accurately presented. However, they are not guaranteed as to the accuracy or completeness and are subject to change without any notice. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have been under or over compensated for the impact, if any, or certain market factors such as liquidity, slippage and commissions. Simulated trading programs, in general, are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any portfolio will, or is likely to achieve profits or losses similar to those shown. All investments and trades carry risk.

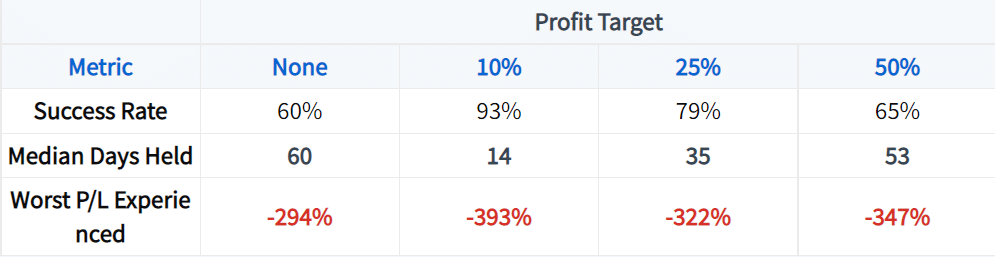

Taking profits at 10-25% of the maximum profit potential significantly increased the consistency of returns relative to not managing trades at all.

Hopefully, you’ve learned a great deal about how simple profit-taking and loss-taking approaches can potentially improve performance when selling straddles.

Now, we’ll examine the historical performance of combining profit targets and stop-losses on short straddle positions.

Study Methodology

Product: S&P 500 ETF (ticker: SPY)

Expiration: Standard monthly cycle closest to 60 days to expiration.

Trade Setup: Sell the at-the-money call and put. One straddle sold for all trades.

Management:

✓ 10% Profit OR 50% Loss

✓ 25% Profit OR 50% Loss

✓ 10% Profit OR 100% Loss

✓ 25% Profit OR 100% Loss

For example, if a straddle was sold for $10 and a trader used the 25% Profit OR 50% Loss management, they’d close the straddle if the price reached $7.50 (a 25% profit) or $15 (a 50% loss).

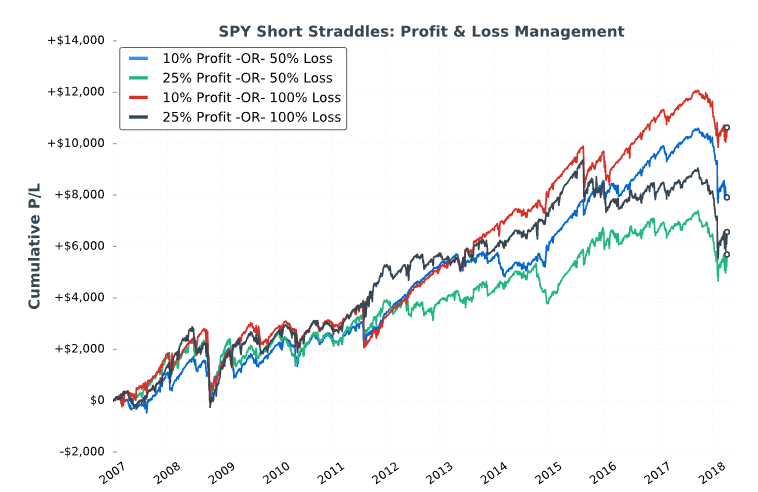

Here were the results of the four short straddle management strategies:

As we can see, all four of the management strategies performed well over the test period, though all strategies suffered major losses in February of 2018.

Consistent with previous findings, the 10% profit target approaches had the smoothest growth curves over time, as short straddles rarely get to higher profit percentages (since that requires the stock price to remain right on the straddle’s strike price as time passes).

As expected, taking profits earlier resulted in higher success rates and fewer days held, but larger drawdowns on the worst trades. The reason is partly because there’s more overall trades when taking profits sooner, but also because the strike price is reset more often.

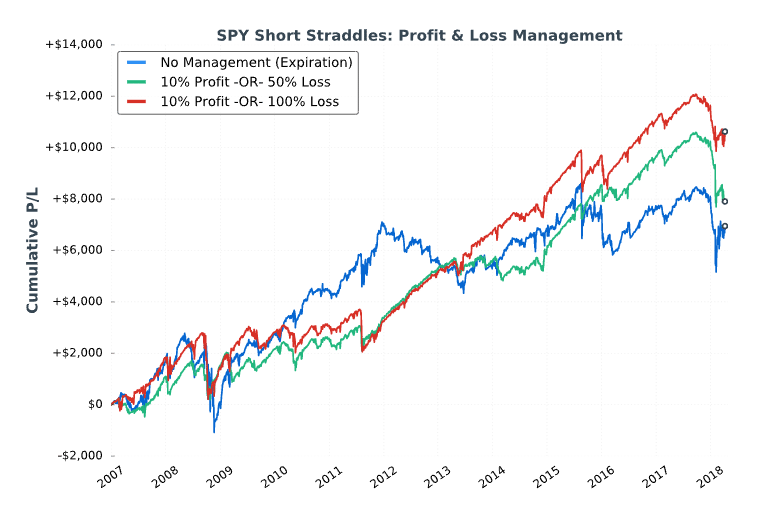

How did the 10% profit-target approaches compare to not managing trades at all?

Holding short straddles to expiration had a period of outperformance between 2009-2012, but lagged behind the management approaches and was much less consistent during the 2012-2018 period.

During the 2009-2012 period, the VIX Index (implied volatility of S&P 500 options) was incredibly high and decreasing quickly in the years after the 2008 market collapse. A quickly decreasing VIX Index is a favorable environment for short premium strategies, as profits can occur very quickly. Consequently, taking small profits lagged behind letting the trades run until expiration.

However, during lower implied volatility environments (such as 2013 to early 2018), taking off profitable trades sooner led to much more consistent results compared to holding to expiration. It makes sense, as the market is typically grinding higher during low implied volatility environments (which is why implied volatility is low).

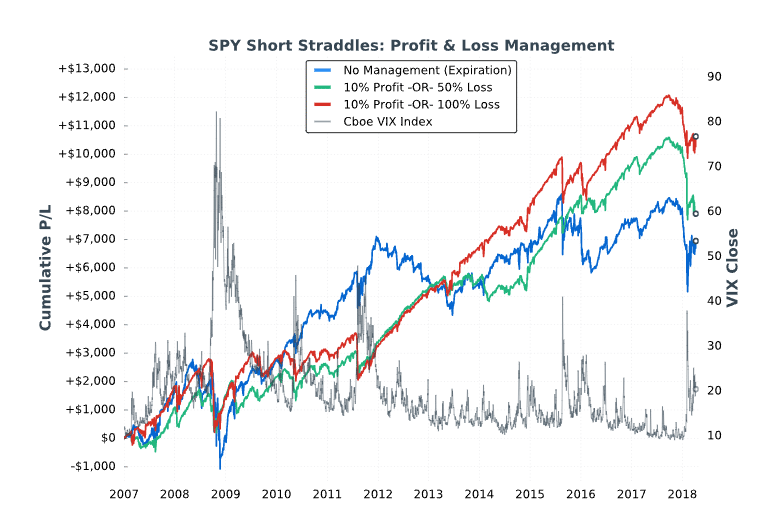

Here’s the same chart from above but with the VIX Index plotted against the strategies:

It’s important to note that while all of the above approaches show profits after the entire test period, all approaches suffered substantial losses at times, especially during February of 2018.

Over a long enough period of time, there will be market crashes worse than what was experienced in 2008, 2015 and 2018.

With that said, short straddles carry substantial risk and should be implemented with extreme caution (if at all). Undefined-risk strategies like short straddles and strangles are far riskier than what most traders are comfortable with, especially when increasing trade size.

Always think about risk before making any trades, and keep in mind that losses can become severe very quickly when selling naked options.